Iron and Steel Overview: Employment and Productivity

Canadian Iron and Steel Industry

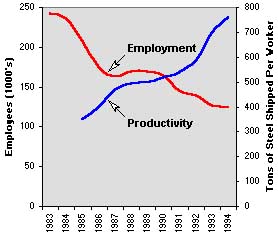

Employment and Productivity

Energy Consumption

Environmental Issues

Industry Modernization and Restructuring

Integrated Mill Business Structure

International Competition

Labor Issues

Market Drivers

Price Trends

Products and Markets

Regulations and NOx Control

Rolling Mills / Secondary Finishing

Sales Revenue and Profitability

Shipments by Major Markets

Shipments by Type of Market

Shipments by Type of Product

U.S. Share of World Output

U.S. Steel Shipments

The number of employees in the steel industry has declined steadily from a high of over 500,000 workers in the early 1970’s to 125,000 in 1994. This structural decline in the industry has effected entire economies of the Midwest and Great Lakes over this period leading to the term “the rust belt” signifying the decline of heavy industry that has characterized the region. Through new technology, capital investment, greater capacity utilization, layout and flow of material, more skillful labor force and management, the steel industry has succeeded in maintaining production with ever smaller number of workers. In 1985, the industry shipped 351 tons of steel for every worker, whereas in 1994, this number had more than doubled to 761 tons/worker.

Annual Statistical Report 1994, American Iron and Steel Institute, Washington D.C. 1995